Portfolio Margining for Interest Rate & Mortgage Futures & Options

March 2025

Portfolio margining is a modern risk management approach that consolidates various positions within a portfolio to offset risks and reduce overall margin requirements. This method is particularly beneficial for derivatives accounts, where long and short positions in different instruments can be netted against each other, resulting in significantly lower margin requirements for hedged positions compared to traditional margin policies. By optimizing portfolio margining, risk managers can achieve substantial capital savings, thereby lowering their cost of capital and improving efficiency for overall financial performance.

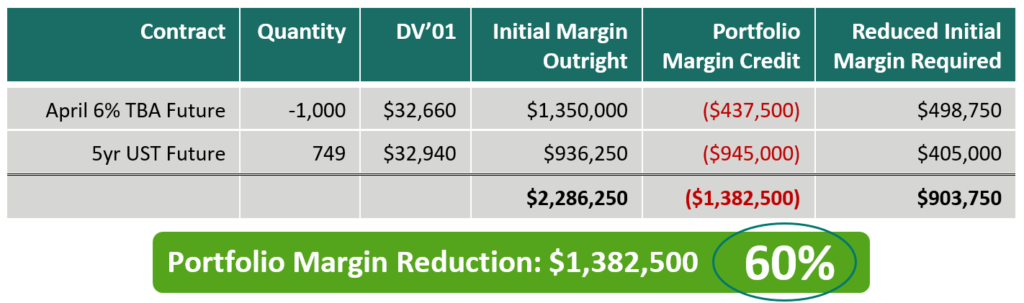

Example 1: TBA vs US Treasury Future

$100MM Notional TBA Future vs Equivalent DV’01 in Offsetting 5yr US Treasury Future

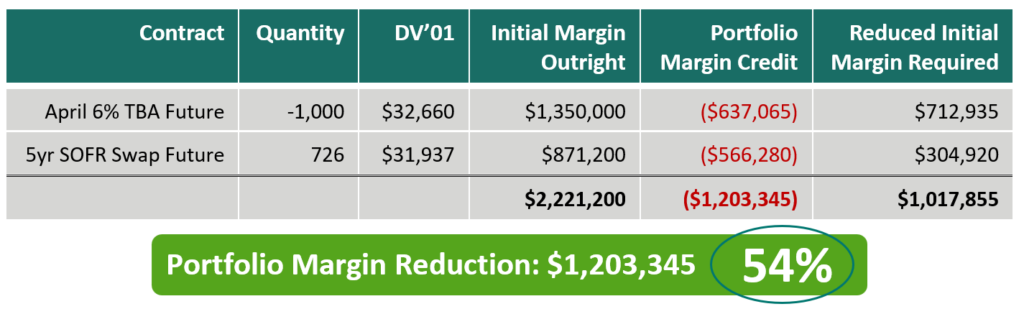

Example 2: TBA vs SOFR Swap Future

$100MM Notional TBA Future vs Equivalent DV’01 in Offsetting 5yr SOFR Swap Future

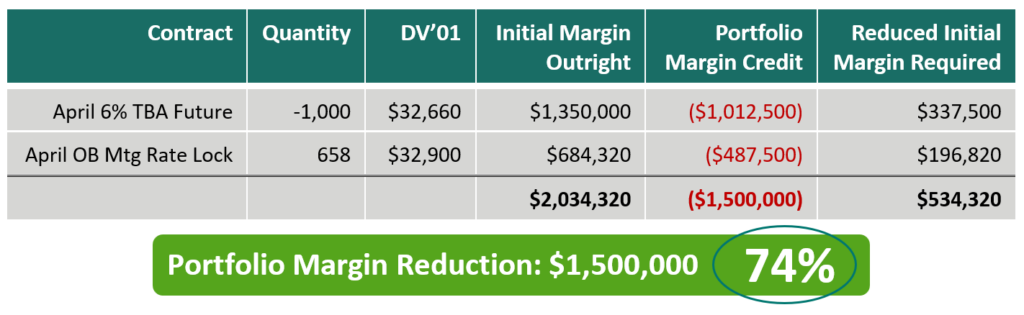

Example 3: TBA vs CME Optimal Blue Mortgage Rate Lock Future

$100MM Notional TBA Future vs Equivalent DV’01 in Offsetting CME Optimal Blue Rate Lock Future

Risk managers hedging separate sides of the portfolio with both long and short hedge positions can take advantage of the portfolio margining benefits automatically applied to derivative hedge positions within the same account at RJ O’Brien. Contact The Fixed Income Group at RJ O’Brien for more information.

**Margin values listed above are reflective of margin requirements as of 3/7/2025 generated from RJO’s Risk Analyzer tool.

The Fixed Income Group at RJO

DISCLAIMER This material has been prepared by a sales or trading employee or agent of R.J. O’Brien and is, or is in the nature of, a solicitation. This material is not a research report prepared by R.J. O’Brien’s Research Department. By accepting this communication, you agree that you are an experienced user of the futures markets, capable of making independent trading decisions, and agree that you are not, and will not, rely solely on this communication in making trading decisions. DISTRIBUTION IN SOME JURISDICTIONS MAY BE PROHIBITED OR RESTRICTED BY LAW. PERSONS IN POSSESSION OF THIS COMMUNICATION INDIRECTLY SHOULD INFORM THEMSELVES ABOUT AND OBSERVE ANY SUCH PROHIBITION OR RESTRICTIONS. TO THE EXTENT THAT YOU HAVE RECEIVED THIS COMMUNICATION INDIRECTLY AND SOLICITATIONS ARE PROHIBITED IN YOUR JURISDICTION WITHOUT REGISTRATION, THE MARKET COMMENTARY IN THIS COMMUNICATION SHOULD NOT BE CONSIDERED A SOLICITATION. The risk of loss in trading futures and/or options is substantial and each investor and/or trader must consider whether this is a suitable investment. Past performance, whether actual or indicated by simulated historical tests of strategies, is not indicative of future results. Trading advice is based on information taken from trades and statistical services and other sources that R.J. O’Brien believes are reliable. We do not guarantee that such information is accurate or complete and it should not be relied upon as such. Trading advice reflects our good faith judgment at a specific time and is subject to change without notice. There is no guarantee that the advice we give will result in profitable trades.

CONTACT

222 South Riverside Plaza, Suite 1200

Chicago IL, 60606

P. (800) 367-3349

fig@rjobrien.com

© 2025 R.J. O'Brien & Associates LLC. | Site by :: kirkgroup

Futures trading involves the substantial risk of loss and is not suitable for all investors. Past performance is not indicative of future results.